By Casey Bell, Sarah Su-Wen Anderson, and Sachi Shenoy

November 2022

Pacific Community Ventures (PCV) is one of the U.S.’s first impact investing organizations, and a community development financial institution (CDFI) with a mission to eradicate the market failures that create barriers for small business entrepreneurs that perpetuate the racial and gender wealth gap in America. PCV provides restorative loans and culturally-competent business advising to its small business clients, and in 2022 launched its Good Jobs Innovation Lab, which leverages data infrastructure and analytics to surface behavioral economic insights and identify drivers of good jobs creation. Over its 20-year history, PCV has invested $35 million and provided over 14,000 hours of advisory services to 3,000 small businesses. A sample of these entrepreneurs reported sustaining 2,882 jobs in 2021, representing 37% of the portfolio.

The age-old question in impact investing – is there a fundamental trade-off between financial return and impact? – is, unsurprisingly, not a straightforward one to answer. Some say it is because impact is notoriously difficult to measure, but we feel the reason is more nuanced: for mission-driven organizations, it may be difficult to measure the degree to which some activities are more impactful than others.

Moreover, the traditional impact frontier comparing impact and return fails to account for societal return. CDFIs were formed to address market failures;yet the racial wealth gap is an intergenerational challenge that has only gotten worse over the decades. Traditional metrics that measure our performance often fail to account for the value created by carving pathways to wealth creation in historically underestimated communities, and mitigating systemic risk to our economy and democracy from recalcitrant racial and gender wealth gaps.

As an anti-racist, impact-first non-profit CDFI, PCV is committed to, and able to, deploy capital at more flexible terms than peer financial institutions, and to more intentionally serving BIPOC, women-identifying, immigrant, and refugee entrepreneurs in under-estimated communities. Partially, as a response to the COVID-19 pandemic, and partially as a launch of its place-based strategy, in late 2021, PCV launched its Oakland Restorative Loan Fund, co-created and deployed with local BIPOC led organizations who know their communities and entrepreneurs best. A total of $2.5 million was deployed to 37 small businesses in the Oakland community, at 0% rates of interest and no fees through that winter.

Feedback from the community was resoundingly positive, and small business owners appreciated the rapid deployment of these loans and 0% interest at a time of great uncertainty. Loans on these terms were a first for PCV, and obviously it would forego any financial return, but the team expected a more significant return on impact than in its traditional portfolio.

To test this hypothesis, PCV plotted the 37 Oakland loans along with 29 loans from a comparison group, comprising its standard loan products (with rates between 3-6.5%), along an impact frontier. The team hypothesized that the comparison group would score higher on financial return, but lower on impact, while the Oakland loans would do the opposite. By creating a scatterplot, the PCV team hoped to identify a “best fit linear relationship” that would quantify the amount of financial return it would have to forego in order to increase impact.

A risk-adjusted financial return was calculated for each loan, using a market default rate for small businesses and probabilities adjusted based on any payment delinquency. An impact score was then calculated for each loan based on a rubric developed by the team to assess impact potential at the time of underwriting, including the following categories (and weights):

- Demographic Equity (50%): Are the business owners and employees from historically underestimated backgrounds?

- Enterprise access to financing (30%): Does this business have access to affordable financing outside of PCV?

- Ability to create good jobs (10%): Does this business have the capacity and willingness to create and maintain quality jobs?

- Customers and community (10%): What is this business’s potential to create a marginal positive impact on its community, society, and the environment?

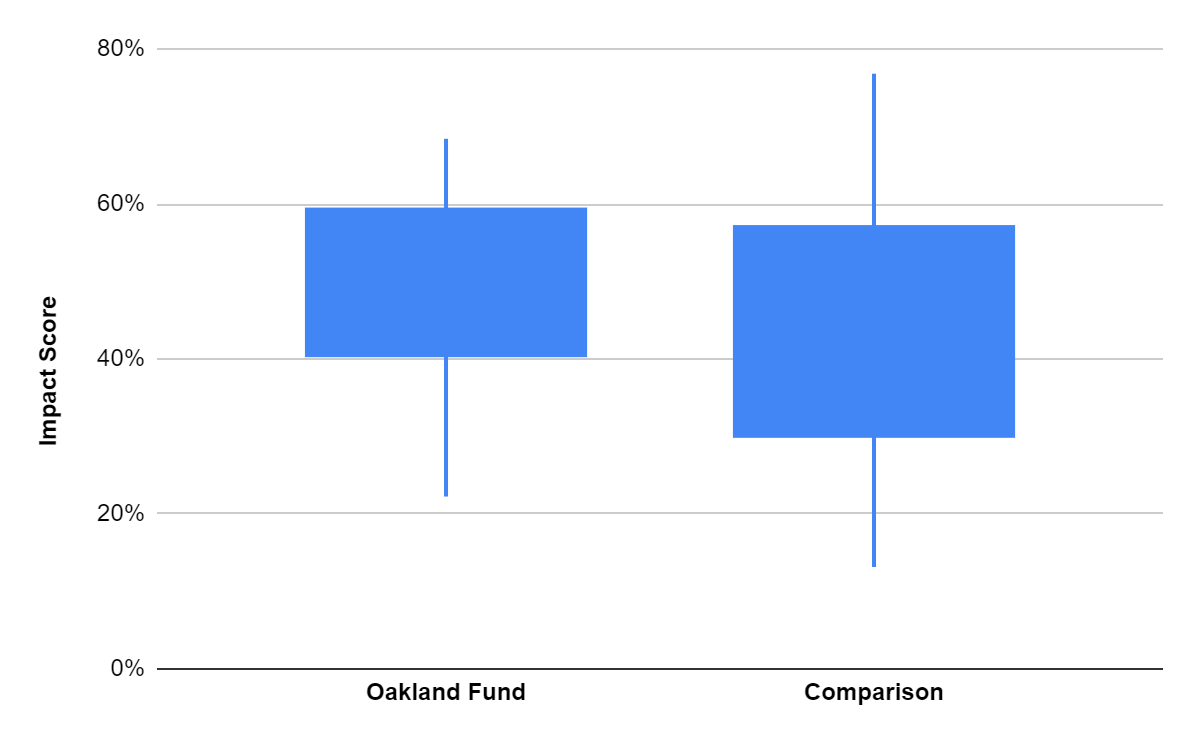

Interestingly, the scatter plot yielded no observable, significant linear relationship between financial return and impact ratings in this small sample. The comparison loans had a positive financial return on average versus the negative returns of the Oakland loans, which was expected; and the median impact scores were 39% versus 46%, respectively.

That said, a simple descriptive measurement of the portfolio showed the place-based portfolio had a higher median impact score and lower variance-suggesting the place-based approach might provide more consistency in delivering impact returns. An observation we look forward to examining more robustly. The Oakland loans scored higher on the dimensions of demographic equity, access to financing, and customers and community, not to mention the savings that accrued to small businesses and loan affordability during economic uncertainty.

In this analysis, PCV did not control for multicollinearity – or relationships between variables within the rubric. The impact scores for both the Oakland loans and the comparison group converged around the same general percentages because even PCV’s “standard” loans are approved based on the same impact framework that prioritizes racial equity and ensuring access to finance. To demonstrate a more stark tradeoff, PCV would have to map loans made without a specific impact intent, at closer to standard market rates. PCV’s mandate to invest for impact challenges its ability to tease apart the different impact variables and test the degree of financial tradeoff necessary to effect deeper impact. In the meantime, the team is committed to expanding its place-based strategy and experimenting with different loan amounts and terms to best support its impact priorities.

Future work may also seek to add a third dimension to the impact frontier analysis – seeking to account for asset creation and risk mitigation through community investment at restorative rates designed to stabilize and build sustainable wealth creation through the small business infrastructure providing essential services to our economy and employing almost half of Americans. We differentiate this axis from “impact” given it focuses less on driving capital to targets, and more on viewing “return” from a different perspective. PCV is dedicated to exploring fresh framing that iterates toward articulating the true value of impact.

Casey Bell is the Chief Impact Officer at Pacific Community Ventures. Sarah Su-Wen Anderson is a PCV intern pursuing dual MBA/MPP degrees at the Stanford Graduate School of Business and the Harvard Kennedy School of Government. Sachi Shenoy is Co-Founder and CEO of Calidris, serving as a Senior Advisor to PCV to glean impactful insights from its data and research agenda centered around good jobs.